Ever wondered how businesses accurately track their expenses for specific projects? Job costing examples are crucial for understanding the financial health of any project. By breaking down costs associated with labor, materials, and overhead, companies can make informed decisions that impact their bottom line.

In this article, you’ll discover various job costing examples across different industries. From construction to manufacturing, each sector utilizes unique methods to ensure profitability and efficiency. Whether you’re a small business owner or a seasoned manager, grasping these concepts will enhance your ability to manage budgets effectively.

Understanding Job Costing

Job costing involves tracking and analyzing costs for specific projects or jobs. It provides a detailed view of how resources are allocated and helps you assess profitability. By breaking down expenses into categories, you gain insights into financial performance.

Definition of Job Costing

Job costing is a method used to assign costs to individual projects or jobs. This includes direct costs like labor and materials, as well as indirect costs such as overhead. For example, in construction, job costing tracks expenses for each building project separately to ensure accurate budgeting.

Importance of Job Costing in Business

Job costing plays a crucial role in managing business finances. It enables you to understand where money goes on each project. Here are key reasons why it matters:

Ultimately, effective job costing supports better decision-making and enhances overall operational efficiency.

Job Costing Examples in Different Industries

Job costing varies significantly across industries, each adopting unique methods to track and manage expenses. Understanding these examples can enhance your ability to implement effective job costing strategies.

Construction Industry

In the construction industry, job costing plays a critical role in project management. Contractors break down costs into several categories:

- Labor Costs: Includes wages for workers directly involved in the project.

- Material Costs: Encompasses all materials required for construction, like concrete and steel.

- Overhead Costs: Accounts for indirect costs such as equipment rental and utilities.

For example, if you’re building a home, you might allocate $150,000 for labor, $100,000 for materials, and $50,000 for overhead. This detailed breakdown helps assess overall profitability.

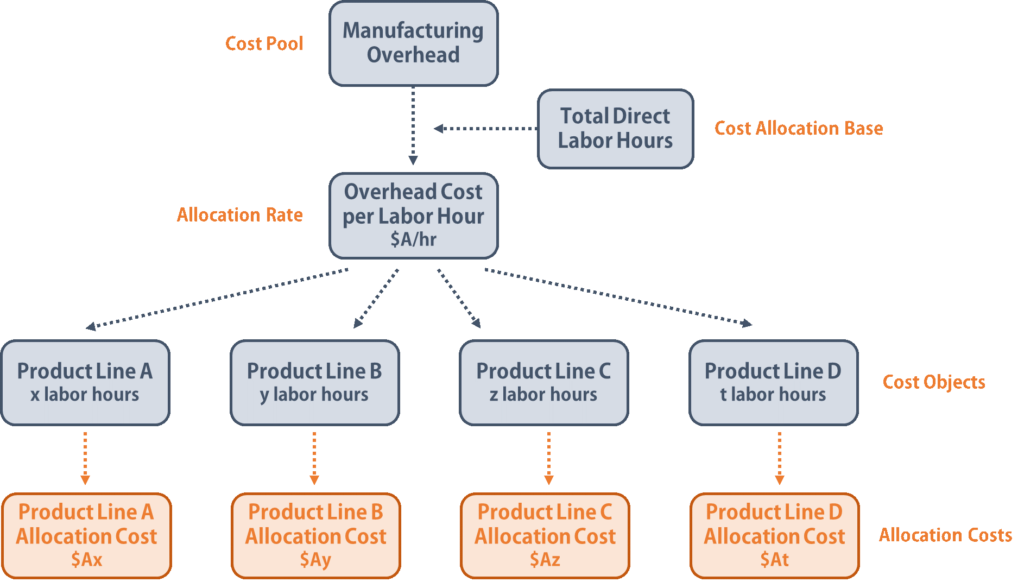

Manufacturing Industry

Manufacturing firms rely on precise job costing to maintain efficiency. The process often includes:

- Direct Materials: Raw materials used in production.

- Direct Labor: Labor costs attributed directly to manufacturing products.

- Manufacturing Overhead: Indirect costs related to production facilities.

Suppose you’re producing furniture; you may spend $20 per chair on direct materials and $15 on direct labor per chair. If overhead is estimated at $5 per chair, understanding these costs allows you to price items effectively while ensuring profitability.

Service-Based Industry

In the service-based industry, job costing focuses on tracking time and resources spent delivering services. Key components include:

- Labor Hours: Total hours worked by employees providing the service.

- Materials Used: Any supplies necessary during service delivery.

- Indirect Costs: Overheads related to administration or facility usage.

For instance, a marketing agency could track 10 hours of labor at $50/hour plus $200 in software subscriptions used for a campaign. Knowing your total cost aids in setting competitive pricing while maintaining profit margins.

Key Components of Job Costing

Job costing breaks down costs into specific components, allowing you to track expenses accurately. Understanding these components is essential for effective budgeting and financial analysis.

Direct Materials

Direct materials refer to the raw materials used in producing a product or completing a project. For example, in construction, if you’re building a house, direct materials include bricks, cement, and wood. In manufacturing furniture, direct materials cover items like fabric and wood. Tracking these costs helps you stay on budget and ensures transparency in your financial reporting.

Direct Labor

Direct labor encompasses the wages paid to workers directly involved in production or service delivery. For instance, a contractor pays carpenters for time spent building structures. In a bakery, direct labor includes wages for bakers preparing goods. Monitoring this cost helps identify inefficiencies and offers insights into labor productivity.

Overhead Costs

Overhead costs consist of indirect expenses related to running your business but not tied directly to any single job. Examples include rent for your office space or utilities necessary for operations. These costs can add up quickly; therefore it’s crucial to allocate them correctly across projects. By understanding overheads better, you can price services competitively while maintaining profit margins.

How to Calculate Job Costs

Calculating job costs involves several steps that ensure accurate tracking of expenses. By following a systematic approach, you can gain clear insights into the financial aspects of your projects.

Collecting Relevant Data

Collecting relevant data is crucial for precise job costing. Start by gathering information on:

- Direct materials: List all raw materials needed for the project. For example, in construction, this could include bricks and cement.

- Direct labor: Document wages of workers directly involved in the task, like electricians or carpenters.

- Overhead costs: Identify indirect expenses such as rent, utilities, and administrative salaries. These affect overall profitability but aren’t tied to a specific job.

Make sure to keep detailed records throughout the project lifecycle. This helps prevent discrepancies later on.

Analyzing Cost Variances

Analyzing cost variances reveals how actual costs compare against your budgeted amounts. Here’s how to do it effectively:

- Calculate total job cost: Sum up direct materials, direct labor, and overhead incurred during the project.

- Compare with estimates: Look at your initial budget versus actual spending. Are there significant differences?

- Identify reasons for variances:

- If material prices increased unexpectedly.

- If labor hours exceeded projections due to delays or inefficiencies.

Understanding these variances enables you to adjust future budgets and improve bidding accuracy while enhancing operational efficiency across projects.