Navigating the world of credit cards can be tricky, especially when you encounter terms like installment and revolving credit. Do you know which one your card falls under? Understanding these concepts is crucial for managing your finances effectively.

In this article, we’ll dive into the differences between credit card installment and revolving options, helping you make informed decisions about your spending habits. You’ll learn how each type affects your budget, payment schedules, and overall financial health.

Understanding Credit Card Payment Structures

Credit cards primarily feature two payment structures: installment credit and revolving credit. Each structure affects your finances differently.

Installment Credit

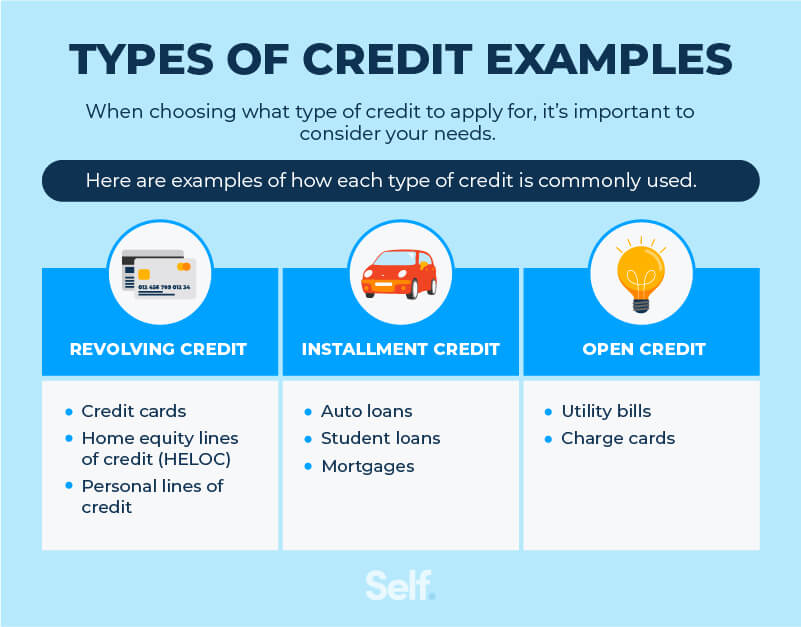

With installment credit, you repay a fixed amount over a specific period. Here are some examples:

- Personal Loans: You borrow a set amount and pay it back in monthly installments.

- Auto Loans: You finance a vehicle’s purchase with fixed monthly payments until the loan is paid off.

- Home Mortgages: You take out a loan to buy property, repaying it over several years with consistent payments.

Installment credit offers predictability in budgeting since you know exactly how much to pay each month.

Revolving Credit

Revolving credit allows you to borrow up to a certain limit, paying down the balance whenever you wish. Consider these examples:

- Credit Cards: You can charge purchases up to your limit and make minimum payments or pay off the full balance.

- Lines of Credit: These provide access to funds which can be drawn upon as needed, similar to checking accounts.

Revolving credit provides flexibility but may lead to higher interest costs if balances remain unpaid for long periods.

Understanding these structures helps in managing your budget effectively. Which option suits your financial needs better?

Credit Card Installment Plans

Credit card installment plans allow you to repay a fixed amount over a specified period. These plans provide structure and predictability in your payments, making budgeting easier.

Definition and Features

Credit card installment plans let you split your purchases into smaller, manageable payments. Typically, these payments occur monthly and span several months or years. You often see this option for larger purchases like electronics or travel expenses. Key features include:

These characteristics ensure clarity in your financial commitments.

Advantages of Installment Plans

Installment plans offer several benefits that enhance financial management. For one, they simplify budgeting since you know exactly how much to pay each month. Additionally, they can help avoid high-interest charges associated with revolving credit by allowing you to pay off your balance without accruing additional debt. Other advantages include:

By choosing an installment plan, you gain control over your finances while making significant purchases more affordable.

Revolving Credit Cards

Revolving credit cards offer flexibility and convenience in borrowing. You can use them for various purchases up to a specific limit, paying off the balance over time while potentially incurring interest on any unpaid amount.

Definition and Features

Revolving credit cards allow you to borrow against a predetermined credit limit. When you make purchases, your available credit decreases. Once you repay part of the balance, your available credit increases again. Key features include:

- Flexible repayment: Pay off the full balance or a minimum monthly payment.

- Credit limits: Limits vary based on your creditworthiness.

- Interest charges: Interest accrues on balances carried beyond the due date.

Advantages of Revolving Credit

Revolving credit offers numerous advantages that can enhance your financial flexibility. Consider these benefits:

- Convenience: Use it for everyday expenses or emergencies without reapplying.

- Building credit history: Responsible use improves your credit score over time.

- Rewards programs: Many cards offer cash back, points, or travel rewards for spending.

You might find revolving credit useful if you prefer managing payments based on your cash flow each month.

Key Differences Between Installment and Revolving Credit

Understanding the differences between installment and revolving credit is crucial for managing your finances effectively. Each type has unique characteristics that can impact your budgeting and spending habits.

Payment Flexibility

Payment flexibility varies significantly between installment and revolving credit. With installment loans, you repay a fixed amount over a set period, ensuring predictable payments. For example, if you finance a car with an auto loan, you’ll make consistent monthly payments until the loan’s term ends.

Conversely, revolving credit offers more freedom. You can borrow up to a specified limit and pay any amount each month, making it adaptable to your financial situation. This means that if an unexpected expense arises, like a medical bill or home repair, you have the option to adjust your payment.

Interest Rates and Fees

Interest rates and fees differ greatly between these two types of credit. Typically, installment loans come with lower interest rates because they’re considered less risky for lenders. For instance, personal loans may range from 5% to 36%, depending on your creditworthiness.

On the other hand, revolving credit often carries higher interest rates. Credit cards usually charge anywhere from 15% to 25%, which can accumulate quickly if balances remain unpaid beyond their due date. Additionally, many revolving accounts include annual fees or late payment charges that can add up over time.

By understanding these key differences in payment flexibility and costs associated with each type of credit, you can make smarter financial decisions tailored to your needs.

Choosing the Right Option for You

Selecting between installment and revolving credit requires careful consideration of your financial situation. Each option presents unique benefits and challenges. Understanding these will help you make a better choice tailored to your needs.

Assessing Your Financial Situation

Begin by evaluating your current budget and expenses. Consider how much disposable income you have each month. Are fixed payments more manageable for you, or do you prefer flexibility? Reflect on factors such as:

- Monthly income: Determine how much money comes in each month.

- Existing debts: Account for any other loans or credit card balances.

- Spending habits: Analyze whether you’re likely to pay off balances quickly.

This assessment helps clarify which credit type aligns with your financial health.

Recommendations for Cardholders

If you’re leaning toward an installment plan, consider using it for larger purchases like appliances or vacations. This approach offers predictable payments without the risk of accumulating high-interest debt.

On the other hand, if you opt for revolving credit, use it wisely. Pay off the balance in full each month to avoid interest charges and build a positive credit history. Look out for rewards programs that enhance your spending experience.

Ultimately, choose what fits best within your lifestyle while keeping a close eye on how each option affects your overall financial picture.