When it comes to managing wealth, understanding inheritance tax is crucial. Have you ever wondered how much your loved ones could owe when inheriting your assets? This often-overlooked aspect of estate planning can significantly impact the financial legacy you leave behind.

In this article, you’ll explore various examples of inheritance tax implications that affect families across the country. From real estate to investments, each scenario highlights the importance of strategizing effectively to minimize tax burdens. You’ll gain insights into how different states approach these taxes and discover tips for navigating them successfully.

By grasping the nuances of inheritance tax, you can make informed decisions that protect your family’s future. Ready to dive deeper into this essential topic? Let’s uncover what you need to know about inheritance tax and its potential effects on your estate planning journey.

Overview of Inheritance Tax

Inheritance tax significantly affects the wealth you leave behind. Different states impose varying rates and exemptions, making it crucial to understand how these taxes work.

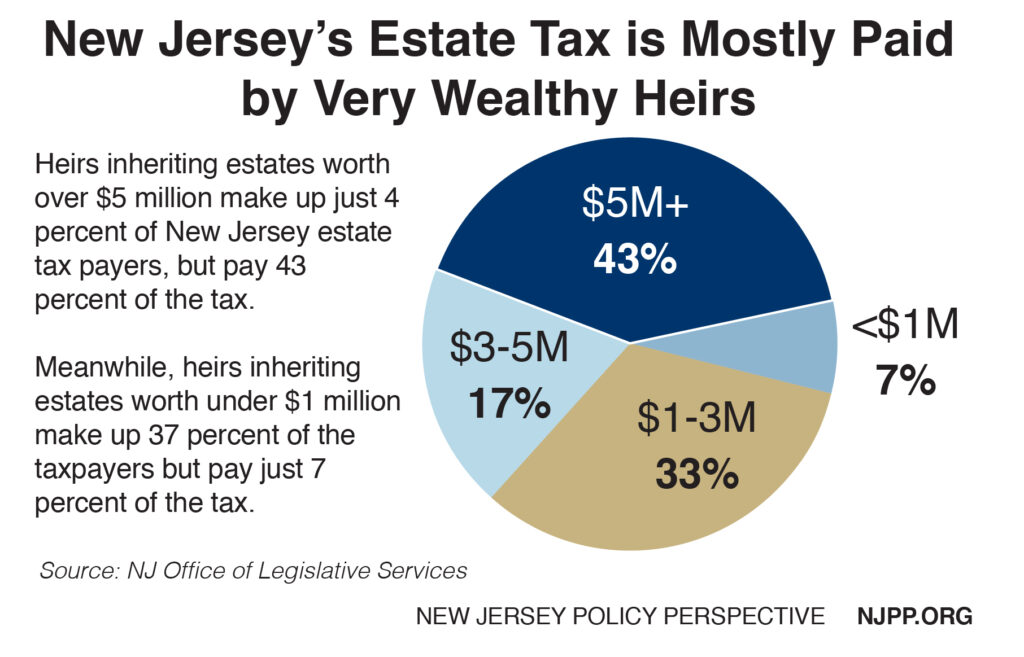

For instance, in California, there’s no inheritance tax. You won’t owe anything if you’re inheriting assets there. However, in New Jersey, the tax can range from 11% to 16%, depending on the relationship between you and the deceased.

Real estate often presents unique challenges. If a loved one leaves property valued at $500,000 and lives in a state with an inheritance tax of 10%, that could mean a $50,000 liability for you.

Investments also incur taxes upon transfer. When inheriting stocks or bonds, their fair market value at the time of death determines your basis. If those assets appreciate over time, you may face capital gains taxes when selling them later.

Life insurance proceeds are typically exempt from income tax. Yet some states include them in the taxable estate value. Thus, understanding local laws is vital to avoid unexpected liabilities.

So what about gifts? Many people confuse gift taxes with inheritance taxes. While gifts during one’s lifetime may affect your taxable estate later on, they typically don’t incur immediate taxation unless they exceed annual limits—$17,000 per recipient as of 2025.

Keeping track of all these factors helps ensure your family inherits as much as possible without unwarranted financial burdens.

Inheritance Tax Laws

Understanding inheritance tax laws is crucial for effective estate planning. These laws vary significantly by state and can greatly affect the financial implications of inheriting assets.

State-Specific Regulations

Inheritance tax is not uniform across the United States. Some states impose this tax, while others do not. For example:

- New Jersey: Rates range from 11% to 16%, depending on your relationship to the deceased.

- Maryland: The inheritance tax rate is 10%, applicable regardless of the beneficiary’s relationship.

- California: There’s no inheritance tax, making it favorable for heirs.

States like Pennsylvania also have varying rates based on familial relationships, which can impact how much you owe upon inheriting property or money.

Federal Guidelines

At the federal level, there isn’t a specific inheritance tax imposed. However, estates exceeding $12.92 million in value face federal estate taxes at rates reaching up to 40%. This threshold applies to individuals who pass away in 2025 and may change with inflation adjustments over time.

Additionally, gifts exceeding $17,000 per person annually count against this exemption limit. Make sure to keep track of any significant gifts made during your lifetime as they could affect your estate’s taxable value later on.

By staying informed about these regulations and guidelines, you can navigate potential pitfalls efficiently and protect your family’s wealth effectively.

Implications of Inheritance Tax

Inheritance tax can significantly affect the financial landscape for heirs. Understanding these implications helps you plan effectively and protect your family’s wealth.

Financial Impact on Heirs

Inheritance tax directly influences how much heirs receive after a loved one’s passing. For example, if an estate valued at $1 million is in New Jersey, heirs might pay between 11% to 16% depending on their relationship to the deceased. This means they could owe up to $160,000 in taxes alone. Additionally, consider Maryland’s flat 10% inheritance tax rate; this impacts both direct descendants and distant relatives equally.

Another aspect involves real estate. If you inherit a property worth $500,000 in Pennsylvania, the tax liability varies based on familial connections—spouses pay less than siblings or cousins. Thus, understanding local laws becomes crucial for accurate financial forecasting.

Estate Planning Considerations

Effective estate planning minimizes inheritance tax burdens and protects assets. You might consider establishing trusts that allow you to transfer assets while avoiding hefty taxes upon death. Trusts can also provide more control over how beneficiaries access inherited wealth.

Moreover, gifting strategies play a role in reducing taxable estates. For instance, gifting amounts below the annual exclusion limit of $17,000 per recipient avoids gift tax implications altogether. Leveraging this strategy allows families to distribute wealth gradually while minimizing future liabilities.

Grasping the nuances of inheritance tax empowers you to make informed decisions that safeguard your family’s financial legacy.

Strategies to Minimize Inheritance Tax

Understanding various strategies can help minimize inheritance tax liabilities. These methods often involve careful planning and legal tools designed to ensure that your loved ones retain more of their inherited assets.

Trusts and Life Insurance

Establishing trusts can significantly reduce inheritance taxes. A trust allows you to transfer assets while avoiding probate, which may incur additional taxes. For example, when you place property into a revocable living trust, it doesn’t count toward your estate’s taxable value upon death.

Additionally, using life insurance strategically can provide liquidity for heirs facing tax bills. If you name beneficiaries directly on the policy, those proceeds typically avoid taxation altogether. This means your family receives the full amount without worrying about immediate tax implications.

Gift Giving and Other Techniques

Implementing a gift-giving strategy helps decrease the size of your estate before death. You can give up to $17,000 per person annually (as of 2025) without incurring gift taxes or affecting your lifetime exemption limit. By spreading out large gifts over several years, you effectively reduce future estate tax burdens.

Other techniques include utilizing 529 plans for education savings or making direct payments for medical expenses on behalf of someone else. Both methods keep those funds outside your taxable estate while benefiting others financially.

In addition, consider charitable contributions during your lifetime. Donating appreciated assets not only reduces the size of your estate but also provides potential income tax deductions based on fair market value at the time of donation.

By employing these strategies thoughtfully, you enhance financial security for your heirs while minimizing their tax obligations.