Understanding the examples of product costs except can be a game-changer for your business decisions. Have you ever wondered what factors truly influence your product pricing? While many focus on direct costs like materials and labor, there’s a whole world of indirect expenses that often go unnoticed.

Definition of Product Costs

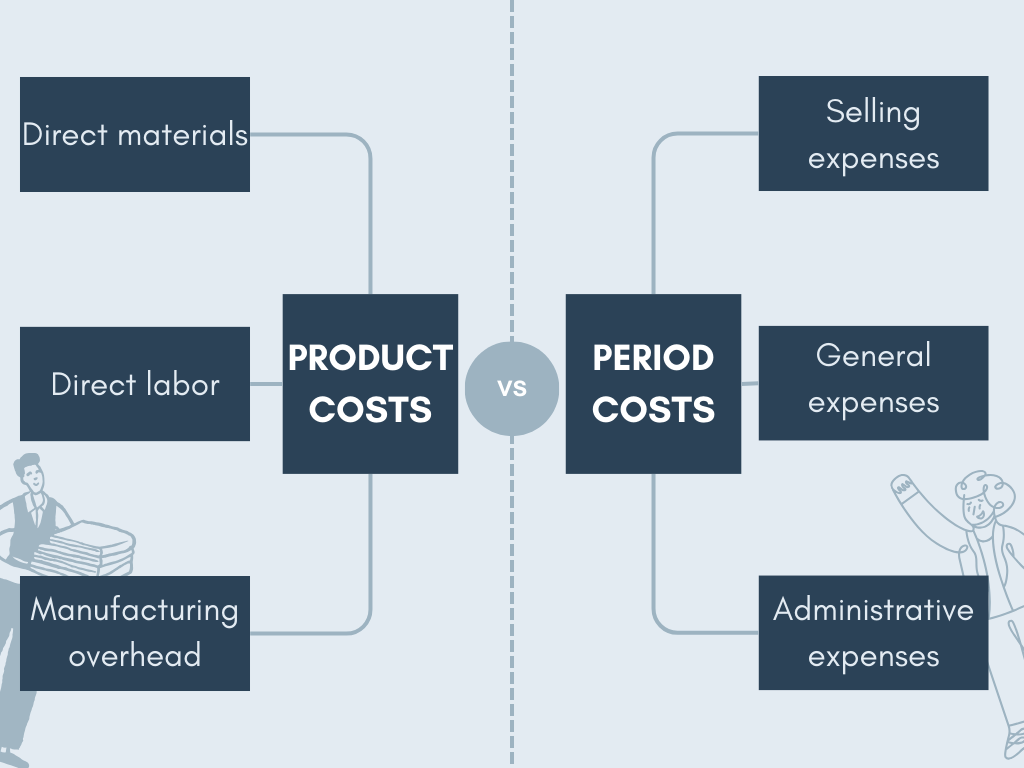

Product costs refer to the total expenses incurred in manufacturing or purchasing a product. Understanding these costs is crucial for pricing strategies and overall financial health. They typically fall into two categories: direct costs and indirect costs.

Direct Costs

Direct costs include expenses that can be directly attributed to the production of goods. Examples are:

- Raw materials: The components used to create a product, like steel for furniture.

- Labor: Wages paid to workers who assemble products.

- Manufacturing supplies: Items necessary for production, like tools.

These costs fluctuate based on production volume, making them essential for budgeting and forecasting.

Indirect Costs

Indirect costs encompass expenses not directly tied to specific products but still impact overall operations. Key examples are:

- Utilities: Electricity and water used in the manufacturing facility.

- Rent: Payments for the space where production occurs.

- Administrative salaries: Wages for staff involved in management rather than hands-on production.

Understanding these indirect expenses helps you assess total cost structures more accurately.

Examples of Product Costs Except

Understanding product costs involves recognizing various examples that contribute to overall expenses. Here are some notable categories:

Labor Costs

Labor costs play a significant role in product pricing. They encompass salaries, wages, and benefits for employees directly involved in production. For example:

- Hourly wages for factory workers

- Salaries for supervisors overseeing production lines

- Overtime pay during peak seasons

These expenses can fluctuate based on labor market conditions and company policies.

Overhead Costs

Overhead costs include indirect expenses essential for maintaining operations but not directly tied to specific products. Key examples include:

- Utilities, such as electricity and water used in manufacturing facilities

- Rent or lease payments for manufacturing space

- Administrative salaries of personnel not directly involved in production

These overheads significantly impact total product cost calculations, influencing your pricing strategies and profit margins.

Importance of Understanding Product Costs

Understanding product costs is vital for effective business management. Accurate knowledge of these costs influences pricing strategies and profit margins. Many businesses overlook indirect expenses, which can significantly affect total product costs. Identifying all components ensures that you set competitive prices while maintaining profitability.

Examples of both direct and indirect product costs include:

- Raw materials: Materials used in production directly impact cost.

- Labor: Salaries for employees involved in manufacturing contribute to overall expenses.

- Utilities: Electricity and water bills are essential but often neglected when calculating product costs.

- Rent: The cost of space used for production affects budgeting decisions.

Recognizing these elements equips you to make informed financial choices. Moreover, it helps in forecasting future expenses accurately. How can you improve your pricing strategy without a complete understanding of what goes into your products?

Common Misconceptions About Product Costs

Many people think product costs only involve direct expenses. However, that’s not true. Indirect costs play a crucial role in determining the total cost of a product. For instance, utilities and rent are often overlooked but significantly affect overall pricing.

You might believe that labor costs are just salaries. In reality, they also include benefits, overtime pay, and training expenses. This comprehensive view of labor costs can change your understanding of profitability.

Some assume all overhead costs are fixed. Yet, many fluctuate based on production levels or seasonal demand. Recognizing this variability helps in creating accurate budgets and forecasts.

It’s common to ignore administrative salaries when calculating product costs. But these salaries contribute to overall business operations and should be considered as part of the total cost structure. This oversight can lead to incorrect pricing strategies.

Lastly, not every material expense appears obvious at first glance. For example, shipping fees and storage costs add up quickly but often go unnoticed during initial calculations. Including these hidden expenses is essential for real profit analysis.