In today’s financial landscape, understanding assets is crucial for building wealth and securing your future. But what exactly qualifies as an asset? From tangible items like real estate and vehicles to intangible ones such as stocks and intellectual property, assets play a vital role in your financial portfolio.

Understanding Assets

Assets play a crucial role in your financial strategy. Recognizing their definition and types can enhance your ability to build wealth effectively.

Definition of Assets

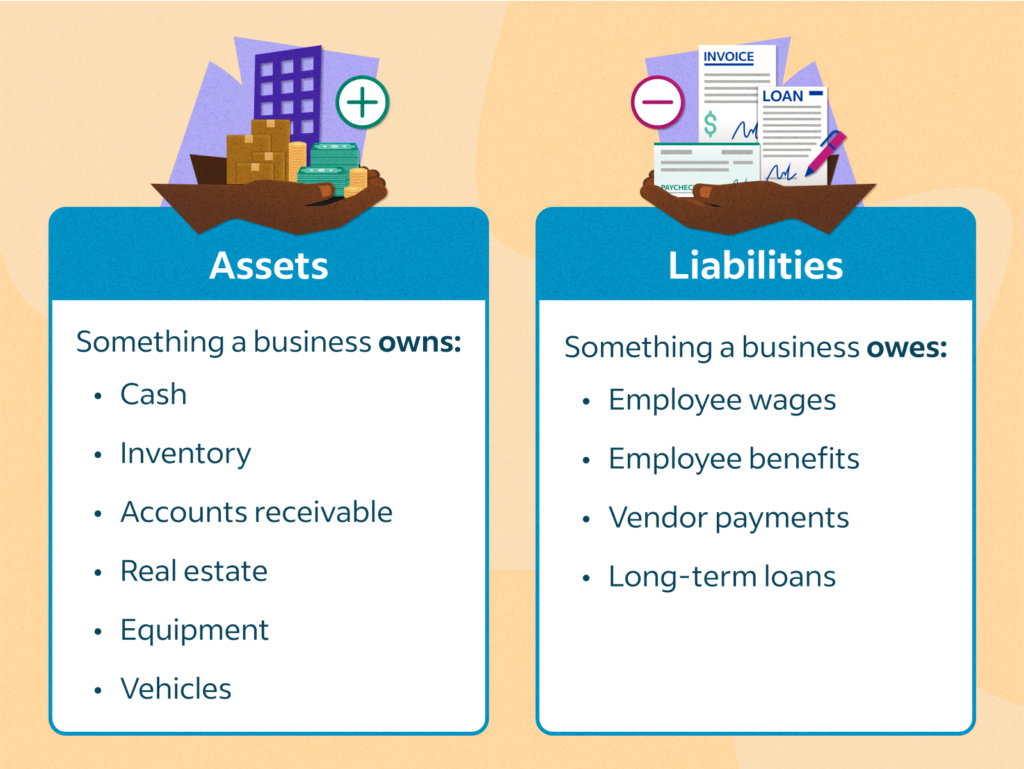

Assets refer to valuable resources owned by an individual or entity. This includes both tangible and intangible items that contribute to your financial status. Tangible assets include real estate, vehicles, and equipment. Intangible assets encompass stocks, patents, and trademarks. Understanding this distinction helps you assess what you own effectively.

Types of Assets

Several categories define the spectrum of assets:

- Current Assets: These are cash or items easily converted into cash within a year, like inventory or accounts receivable.

- Fixed Assets: Long-term resources such as buildings, machinery, and land fall under this category.

- Intangible Assets: Non-physical items like intellectual property rights or brand recognition are crucial for many businesses.

- Financial Assets: Stocks, bonds, and mutual funds represent ownership claims on resources that generate income.

By categorizing your assets this way, you can better understand their value and how they fit into your overall financial picture.

Importance of Assets

Assets play a crucial role in achieving financial goals. They enhance your financial stability and contribute significantly to wealth accumulation. Understanding their importance helps you make informed decisions about managing your finances.

Financial Stability

Financial stability relies heavily on the presence of diverse assets. Without assets, you may struggle during unexpected financial hardships. For instance, having cash reserves or real estate provides a safety net during emergencies. Additionally, investments like stocks can generate passive income, further enhancing your security.

- Emergency Fund: Cash savings can cover 3-6 months of living expenses.

- Real Estate: Property values often appreciate over time.

- Stocks and Bonds: These can provide dividends and interest income.

By maintaining a balanced asset portfolio, you ensure that you’re prepared for life’s uncertainties.

Wealth Accumulation

Wealth accumulation is directly tied to the growth of your assets. The more valuable assets you possess, the greater your potential for building wealth over time. Investing in stocks or mutual funds often leads to compounding returns that significantly increase your net worth.

- Investing Early: Starting young allows compound interest to work in your favor.

- Diversification: Spreading investments reduces risk while maximizing growth potential.

- Retirement Accounts: Contributing regularly boosts long-term savings through tax advantages.

Focusing on accumulating diverse assets positions you for future financial success and independence.

Managing Assets

Managing assets effectively is crucial for financial success and stability. It involves strategic planning, allocation, and monitoring of various asset types to achieve your financial goals.

Asset Allocation Strategies

Asset allocation strategies help you distribute investments among different asset classes. Here are some common approaches:

- Strategic Allocation: This long-term strategy maintains a fixed percentage in each asset class. For example, you might allocate 60% to stocks and 40% to bonds.

- Tactical Allocation: This approach allows for short-term adjustments based on market conditions. You could increase stock holdings during bullish markets.

- Dynamic Allocation: With dynamic allocation, you adjust your investment mix as market conditions change. If stocks decline significantly, you might shift more funds into safer assets like cash or bonds.

Choosing the right strategy depends on your risk tolerance and investment horizon.

Risk Management in Asset Management

Risk management in asset management focuses on minimizing potential losses while maximizing returns. Consider these key practices:

- Diversification: Spreading investments across various sectors reduces the impact of underperforming assets.

- Regular Review: Periodically reviewing your portfolio helps identify areas needing adjustment based on performance or life changes.

- Setting Limits: Establish stop-loss orders to protect against significant losses in volatile markets.

By implementing these tactics, you can better manage risks associated with your assets while working towards your financial objectives.

Evaluating Assets

Evaluating assets involves determining their worth and understanding their role in your financial portfolio. This process aids in making informed decisions that align with your financial goals.

Methods of Valuation

You can use several methods to evaluate assets effectively:

- Cost approach: This method calculates the asset’s value based on the cost to replace it, minus depreciation. For instance, if you own a vehicle worth $20,000 when new but has depreciated to $12,000, its current value is $12,000.

- Market approach: Using this method requires comparing similar assets that recently sold. If comparable homes in your neighborhood sell for around $300,000, it helps determine your property’s market value.

- Income approach: This valuation focuses on estimating future income streams generated by an asset. If a rental property generates monthly rent of $2,000 with expenses of $500, you calculate its annual income as ($2,000 – $500) x 12 = $18,000.

These methods provide insights into how much an asset contributes to overall wealth.

Common Mistakes in Asset Evaluation

Individuals often make mistakes during asset evaluation:

- Ignoring depreciation: Failing to account for wear and tear can lead to overestimating an asset’s value. Always consider how age affects worth.

- Overlooking market trends: Not staying updated on market conditions may skew evaluations. Trends like rising interest rates or housing shortages impact property values significantly.

- Relying solely on one valuation method: Depending only on one approach might yield inaccurate results. Combining multiple methods leads to a more accurate assessment.

By avoiding these pitfalls and employing various strategies for evaluation, you enhance your understanding of each asset’s true value and contribution to your financial landscape.