Accrued liabilities can often leave you scratching your head, especially when determining their classification. Are accrued liabilities current liabilities? This question is crucial for understanding your business’s financial health and ensuring accurate reporting.

In this article, we’ll dive into the nuances of accrued liabilities, exploring how they fit into the broader category of current liabilities. You’ll discover real-world examples that clarify these concepts and help you make informed decisions about your financial statements.

Understanding Accrued Liabilities

Accrued liabilities represent obligations that a business has incurred but hasn’t yet paid. Recognizing these liabilities is crucial for accurate financial statements and understanding overall financial health.

Definition of Accrued Liabilities

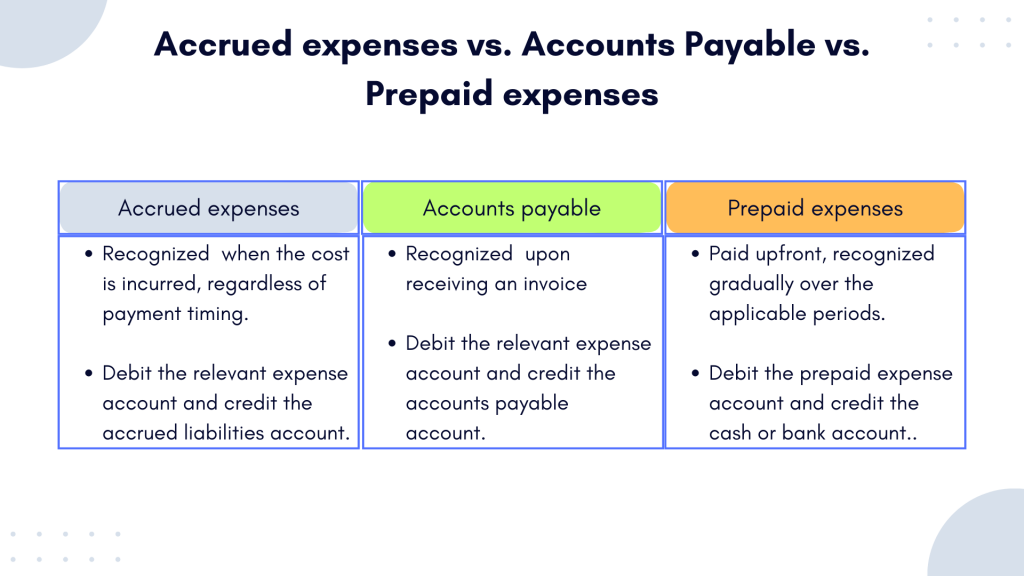

Accrued liabilities are expenses recognized on the balance sheet before they’re paid. For example, when you receive services in December but pay for them in January, this creates an accrued liability. These liabilities ensure that your financial statements reflect the true economic activity during a specific period.

Types of Accrued Liabilities

Several common types exist within accrued liabilities:

- Salaries Payable: Wages earned by employees but not disbursed at the end of an accounting period.

- Interest Payable: Interest on loans or bonds that accumulates over time but hasn’t been paid.

- Taxes Payable: Taxes owed to government entities based on current earnings but not yet remitted.

Current Liabilities Explained

Current liabilities represent short-term obligations a business must settle within one year. Understanding these liabilities is crucial for evaluating financial health and liquidity.

Definition of Current Liabilities

Current liabilities are debts or obligations that a company expects to pay off within a year. These include various types of financial commitments, such as loans, accounts payable, or accrued expenses. Recognizing current liabilities helps businesses manage cash flow effectively and ensures they can meet their short-term financial responsibilities.

Examples of Current Liabilities

Several examples illustrate what qualifies as current liabilities:

- Accounts Payable: This includes unpaid bills from suppliers for goods or services received.

- Short-Term Loans: Any loans due within the next 12 months fall under this category.

- Accrued Liabilities: Expenses incurred but not yet paid, like wages owed to employees at the end of an accounting period.

- Unearned Revenue: Money received before delivering goods or services creates an obligation to fulfill those orders.

- Current Portion of Long-Term Debt: This represents the part of long-term debt that’s due within the next year.

These examples highlight how diverse current liabilities can be. They play a vital role in assessing your company’s operational efficiency and liquidity position.

The Relationship Between Accrued Liabilities and Current Liabilities

Accrued liabilities play a crucial role in financial statements, closely linking them with current liabilities. Understanding this relationship enhances your grasp of a business’s short-term obligations.

Are Accrued Liabilities Current Liabilities?

Yes, accrued liabilities are classified as current liabilities. They represent obligations that you incur but haven’t yet paid by the end of an accounting period. Since these debts typically settle within one year, they fall under the umbrella of current liabilities on the balance sheet. For instance, if your company owes salaries for December but pays them in January, those unpaid salaries are accrued liabilities and count as current liabilities.

Accounting Treatment of Accrued Liabilities

The accounting treatment for accrued liabilities involves recognizing expenses before cash payment. This process ensures your financial statements reflect accurate information about what you owe. When recording an accrued liability, you increase both the expense account and the corresponding liability account.

For example:

- Salaries Payable: If employees worked in December but get paid in January, you record salaries payable at month-end.

- Interest Payable: If your business has loans accruing interest by year-end but hasn’t made payments yet, record that interest as payable.

- Taxes Payable: If taxes accrued during a quarter remain unpaid at quarter-end, list those amounts as accrued tax liabilities.

By understanding these examples and their implications on current liabilities, you can better assess a company’s financial position.

Implications for Financial Reporting

Understanding the implications of accrued liabilities on financial reporting is crucial. These liabilities directly affect how stakeholders perceive a company’s financial health.

Importance in Balance Sheets

Accrued liabilities play a significant role in balance sheets. They appear under current liabilities, impacting your business’s short-term financial position. For example, if your company has unpaid salaries at the end of an accounting period, this obligation must be recorded as an accrued liability. This ensures that your balance sheet reflects all outstanding obligations accurately.

Moreover, recognizing accrued liabilities promotes transparency. Stakeholders can better assess liquidity and operational efficiency when they have complete visibility into all obligations incurred by the business.

Impact on Cash Flow Statements

Accrued liabilities also influence cash flow statements. When you incur expenses but don’t pay them immediately, there’s no cash outflow recorded yet. Despite this absence of cash transactions currently, these liabilities will eventually impact future cash flows when payments are made.

For instance, if you accrue interest payable during one period but pay it in the next, it shows up as an outflow in subsequent periods. This timing difference affects how you forecast cash needs and manage working capital effectively.

Recognizing accrued liabilities impacts both balance sheets and cash flow statements significantly—ensuring accurate representation of your company’s financial activities is essential for informed decision-making.