Have you ever wondered how businesses ensure their financial statements are accurate? Analytical procedures play a crucial role in this process, serving as a powerful tool for auditors and accountants alike. These techniques help identify trends, anomalies, and potential areas of risk by analyzing financial data in relation to expected outcomes.

Overview of Analytical Procedures

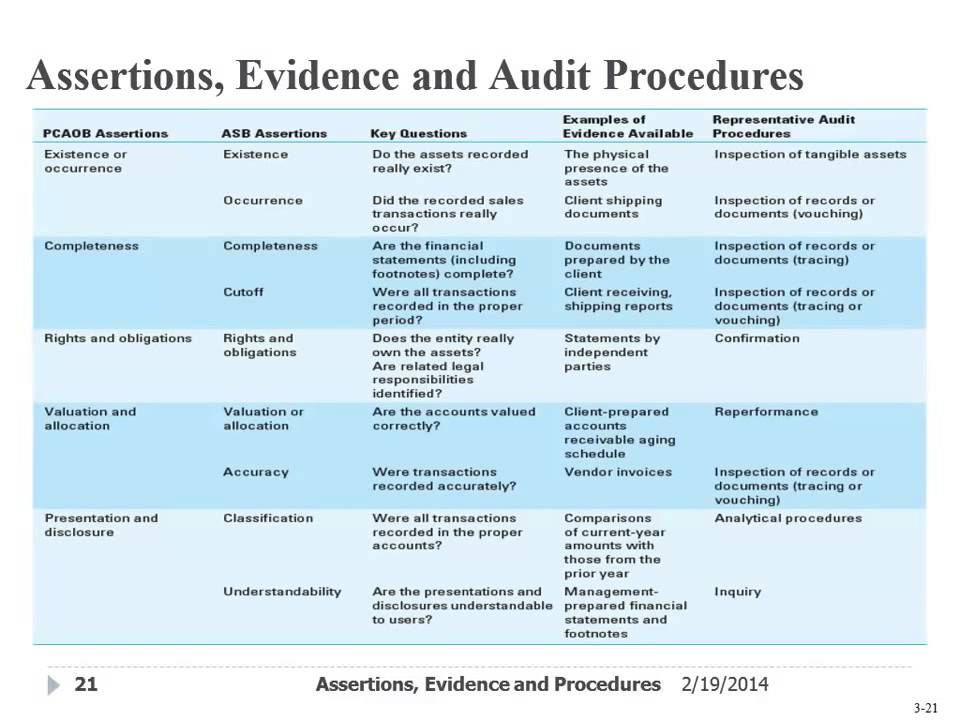

Analytical procedures involve assessing financial information through comparisons and relationships. These techniques assist auditors in identifying areas requiring further investigation.

For example, trend analysis examines financial data over time to spot significant fluctuations. By comparing current year figures to those from previous years, you can uncover unusual changes.

Ratio analysis is another common procedure that analyzes relationships between different financial statement items. For instance, the current ratio indicates a company’s ability to meet short-term obligations by comparing current assets to current liabilities.

Reasonableness tests evaluate whether account balances appear plausible based on expected results. If sales revenue dramatically increases without a corresponding rise in accounts receivable, it may raise red flags.

You might also consider vertical and horizontal analyses. Vertical analysis expresses each item as a percentage of a base figure within a single period, while horizontal analysis compares line items across multiple periods.

Overall, these examples illustrate how analytical procedures provide insights into the reliability of financial statements by spotting trends and discrepancies effectively.

Types of Analytical Procedures

Analytical procedures are crucial for evaluating financial data. They help identify trends and anomalies that may signal potential issues. Here are the main types of analytical procedures used in financial assessments.

Substantive Analytical Procedures

Substantive analytical procedures utilize specific expectations about account balances or transactions to evaluate their reasonableness. For example, you might compare current year sales figures against prior years’ data. This comparison can highlight unexpected changes, indicating areas needing further investigation.

- Trend Analysis: This technique examines patterns over time, such as quarterly revenue growth rates.

- Ratio Analysis: You assess relationships between financial statement items—like comparing net income to total assets.

- Reasonableness Testing: This involves assessing whether account balances make sense based on historical trends or industry norms.

Evaluative Analytical Procedures

Evaluative analytical procedures focus on overall financial performance rather than specific accounts. They aim to understand broader relationships within the financial statements.

For instance, you might analyze operating expenses as a percentage of sales over several periods to determine consistency.

- Vertical Analysis: This method expresses each item on a single financial statement as a percentage of a base figure (e.g., total revenue).

- Horizontal Analysis: This compares line items across periods to spot significant changes.

By applying these methods, you gain valuable insights into business operations and underlying trends affecting performance.

Importance of Analytical Procedures

Analytical procedures play a crucial role in assessing the accuracy and reliability of financial statements. These techniques enable auditors and accountants to identify trends, anomalies, and potential risks by comparing financial data against expected outcomes.

Risk Assessment

Analytical procedures assist in risk assessment by highlighting areas that may warrant further investigation. For example, when you compare current year revenue figures with prior years, significant discrepancies might indicate potential issues. This process allows for early identification of risks related to misstatements or operational inefficiencies.

Fraud Detection

Fraud detection benefits significantly from analytical procedures as well. By applying ratio analysis, you can spot unusual ratios that deviate from industry norms. For instance, if a company’s gross profit margin suddenly drops while expenses remain constant, this could signal fraudulent activities. Such insights prompt deeper investigations into specific transactions or account balances to ensure integrity in financial reporting.

Guidelines for Implementing Analytical Procedures

Implementing analytical procedures effectively enhances the accuracy of financial assessments. Following specific guidelines ensures these techniques yield reliable results.

Planning and Design

Start by defining objectives clearly. Establish what you aim to achieve with analytical procedures, whether it’s identifying trends or assessing risks. Then, select relevant data for analysis. Ensure that the financial information is accurate and up-to-date.

Next, choose appropriate analytical methods tailored to your goals:

- Trend Analysis: Examine financial data over time.

- Ratio Analysis: Analyze relationships between key figures.

- Reasonableness Tests: Evaluate account balances’ plausibility.

These methods help in forming a solid foundation for your analysis.

Execution and Documentation

Execute your analytical procedures systematically. Collect data, conduct analyses, and document findings thoroughly. Ensure that you maintain detailed records of calculations and assumptions made during the process.

While analyzing data:

- Compare current results against historical benchmarks.

- Identify significant deviations from expectations.

- Highlight any unusual patterns or discrepancies.

Documentation not only supports conclusions but also aids in future reference or audits, reinforcing transparency throughout the process.

Challenges in Analytical Procedures

Analytical procedures face several challenges that can impact their effectiveness. Understanding these challenges is crucial for accurate financial assessments.

- Data Quality: Inaccurate or outdated data can lead to misleading conclusions. If the information isn’t reliable, any analysis based on it becomes questionable.

- Complex Financial Structures: Companies with intricate financial systems present difficulties in identifying trends or anomalies. Complexity can obscure meaningful insights.

- Overreliance on Historical Data: While historical data provides a baseline, relying solely on it might ignore current market conditions or operational changes. Context matters significantly.

- Subjectivity in Interpretation: Different analysts may interpret results variably, leading to inconsistent conclusions. This subjectivity can complicate decision-making processes.

- Lack of Skilled Personnel: Limited availability of trained professionals who understand analytical techniques hinders effective implementation and interpretation. Skill gaps affect overall analysis quality.

You might wonder how these challenges affect audit outcomes. Each issue compounds the risk of incorrect assessments, which could ultimately mislead stakeholders regarding a company’s financial health. Addressing these challenges proactively ensures more reliable and insightful analyses.