Mastering the art of adjusting journal entries is essential for anyone serious about accounting. Have you ever wondered how businesses maintain accurate financial records? These entries ensure that your financial statements reflect true economic reality, capturing all transactions that might otherwise go unnoticed.

Understanding Adjusting Journal Entries

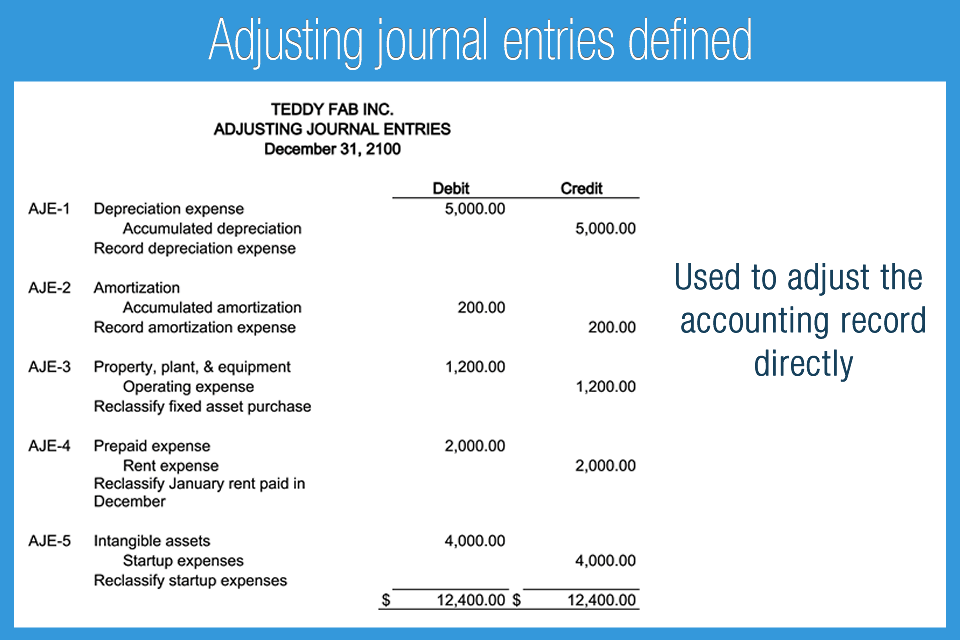

Adjusting journal entries play a vital role in ensuring accurate financial reporting. They capture transactions that may not be recorded during the initial entry, allowing your financial statements to reflect true economic conditions.

Definition and Purpose

Adjusting journal entries are accounting entries made at the end of an accounting period. They correct or update account balances before preparing financial statements. For example, if you incurred expenses but haven’t received an invoice yet, you’d create an adjusting entry to recognize that expense. This entry allows for accurate representation of expenses in your accounts.

Importance in Financial Reporting

Adjusting journal entries enhance the accuracy of financial reports. Without them, your income statement and balance sheet might misrepresent your business’s financial health. Consider these points:

- Accruals: Recognize revenue earned or expenses incurred before cash changes hands.

- Deferrals: Adjust for prepaid expenses or unearned revenue to align with actual performance.

- Estimates: Account for depreciation or bad debts based on predictions about asset value.

These adjustments ensure stakeholders receive reliable information for decision-making.

Types of Adjusting Journal Entries

Adjusting journal entries fall into three main categories: accruals, deferrals, and estimates. Each category serves a specific purpose in financial accounting.

Accruals

Accruals involve recording revenues or expenses that have occurred but haven’t yet been documented in the accounts. For example, if your company provides services in December but won’t receive payment until January, you create an adjusting entry for the revenue earned in December. This ensures that your financial statements accurately reflect income during that period. Another instance includes recognizing wages owed to employees at the end of a month when payday occurs the following month.

Deferrals

Deferrals refer to postponing recognition of certain revenues or expenses until a future date. A common example is prepaid insurance; if you pay for a one-year policy upfront, you’ll adjust entries monthly to recognize one-twelfth of the expense each month rather than all at once. Similarly, consider unearned revenue: if customers pay in advance for services not yet delivered, you’ll record it as a liability and adjust it to revenue as services are performed over time.

The Process of Making Adjusting Journal Entries

Making adjusting journal entries involves several steps that ensure financial records remain accurate and up-to-date. This process requires careful identification, documentation, and recording of necessary adjustments.

Identifying the Need for Adjustments

Identifying when to make adjustments is crucial. You might need to adjust entries if:

- Expenses incurred: If you’ve incurred expenses but haven’t recorded them yet, such as wages earned by employees at the end of a period.

- Revenue recognition: When services are provided in one period but payment arrives later, like completing a project in December while receiving payment in January.

- Prepaid expenses: If you paid for an insurance policy upfront but need to recognize the expense monthly.

Each situation calls for specific attention to ensure accurate financial reporting.

Documenting the Adjustments

Documenting each adjustment accurately maintains clear records. You’ll want to follow these steps:

- Create a journal entry: Write down your adjusting entry with details like date, accounts affected, and amounts.

- Reference supporting documents: Attach invoices or receipts that support your adjustment, ensuring transparency.

- Use consistent terminology: Keep descriptions clear and straightforward so anyone reviewing can easily understand the purpose of each adjustment.

This meticulous approach helps maintain clarity in your accounting practices and supports reliable financial statements.

Common Examples of Adjusting Journal Entries

Adjusting journal entries help maintain accurate financial records. Here are some common examples that illustrate the different types.

Accrued Expenses

Accrued expenses represent costs incurred but not yet paid or recorded. Imagine you’ve received services in December, but the invoice arrives in January. You need to recognize this expense for December to reflect true financial performance.

For instance:

- Utilities Expense: If you used electricity in December, record an accrued utility expense.

- Wages Payable: If employees worked during the last week of December but will be paid in January, recognize their wages as an accrued expense.

This ensures your income statement accurately reflects all expenses for the period.

Unearned Revenue

Unearned revenue occurs when cash is received before services are performed or goods delivered. This liability must be adjusted once the service is completed or goods are delivered.

Consider these examples:

- Subscription Services: If a customer pays for a yearly subscription upfront, adjust unearned revenue monthly as you provide each month’s service.

- Gift Cards Sold: When customers buy gift cards, record this as unearned revenue until they redeem them.

These adjustments ensure that revenue recognition aligns with actual delivery of goods or services, enhancing clarity in your financial statements.