Imagine having a reliable way to calculate how much your investments will grow over time. The future value of annuity formula can be your key to unlocking that potential. Whether you’re planning for retirement or saving for a major purchase, understanding this formula gives you a clearer picture of your financial future.

In this article, you’ll discover how the future value of annuity formula works and why it’s essential for effective financial planning. You’ll explore practical examples that illustrate its application in real-life scenarios. Have you ever wondered how small, regular contributions can accumulate into a substantial sum? By mastering this concept, you can make informed decisions about your savings strategies and investment choices.

Understanding Annuities

An annuity represents a series of payments made at equal intervals. You can encounter them in various financial scenarios, such as retirement plans or insurance products.

An annuity can provide consistent income, especially during retirement. This ensures that you have funds available over an extended period.

You might find two primary types of annuities: fixed and variable. A fixed annuity guarantees a specific payout amount, while a variable annuity’s payout fluctuates based on the performance of underlying investments.

Consider this example: If you invest $100,000 in a fixed annuity with an annual interest rate of 5% for 10 years, your total payout could grow significantly by the end of that term. Want to see how it works?

Here’s how payouts might look:

| Year | Payment Amount |

|---|---|

| 1 | $5,000 |

| 2 | $5,250 |

| 3 | $5,512 |

| … | … |

| 10 | $16,288 |

This demonstrates the power of compounding interest. Each year builds upon the last year’s total.

Moreover, understanding the time value of money helps clarify why starting early is crucial. The sooner you begin contributing to an annuity, the more substantial your future payouts could be.

Wouldn’t it be worthwhile to evaluate different options available? Comparing offers from various providers ensures you secure the best terms possible for your financial goals.

The Future Value of Annuity Formula

The future value of annuity formula calculates the total value of a series of equal payments at a specified interest rate over time. Understanding this formula helps you anticipate how much your regular contributions can grow, guiding your financial planning effectively.

Definition and Importance

The future value of annuity refers to the amount accumulated after making regular payments into an investment account that earns interest. This concept is vital for retirement planning. It allows you to estimate how much money you’ll have when you retire or reach other financial goals. Knowing this figure supports better decision-making regarding savings strategies and investment options.

Components of the Formula

The formula for calculating the future value of an annuity consists of three main components:

- Payment Amount (PMT): This represents each payment made during the investment period.

- Interest Rate (r): This is the annual interest rate, expressed as a decimal.

- Number of Payments (n): This indicates how many times payments are made within a specified timeframe.

You can express it with this formula:

[ FV = PMT times frac{(1 + r)^n – 1}{r} ]

Here’s what happens when you plug in some numbers:

- For instance, if you contribute $200 monthly into an account with a 5% annual interest rate for 20 years, you’d calculate:

- (PMT = 200)

- (r = 0.05/12) (monthly interest)

- (n = 20 times 12) (total monthly payments)

This setup demonstrates how consistent contributions can lead to significant growth over time through compounding returns.

Applications of the Future Value of Annuity Formula

The future value of annuity formula serves multiple practical applications, especially in financial planning and investment decision-making. Here are some key areas where this formula can be effectively utilized.

Retirement Planning

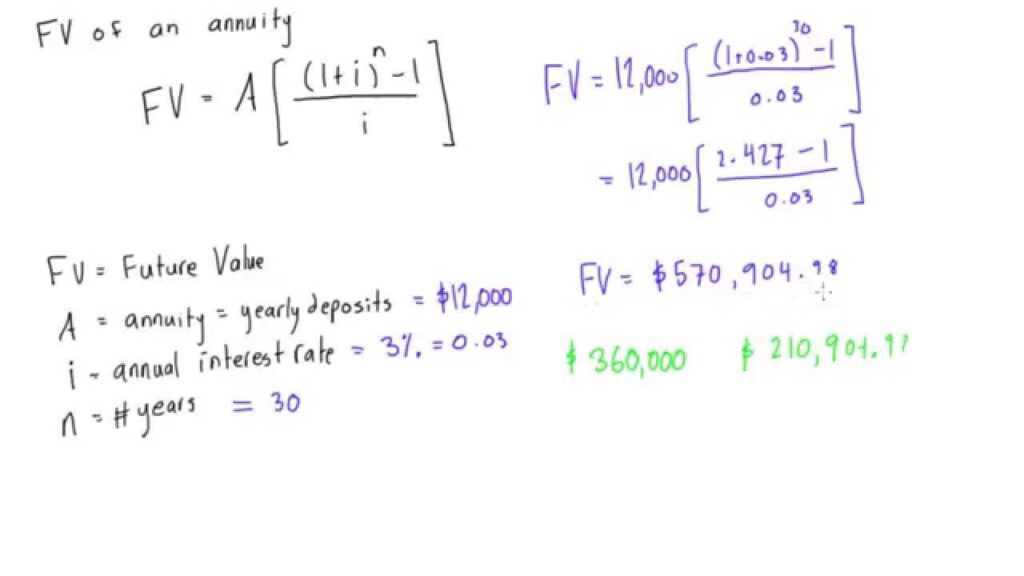

Retirement planning often relies on the future value of annuity formula to estimate your savings growth. For instance, if you plan to retire in 30 years and contribute $500 monthly into a retirement account with a 6% annual interest rate, you could accumulate approximately $570,000 by retirement. Using the formula helps you visualize how consistent contributions lead to substantial funds for your golden years.

Investment Decisions

Investment decisions benefit greatly from understanding the future value of annuities. Consider you’re evaluating two investment options: one offers a fixed monthly contribution of $300 at 5% annual interest over 15 years, while another provides variable returns at an average of 8%. Calculating the future values allows you to compare potential outcomes and select investments that align with your financial goals more effectively.

Additionally, tracking different scenarios helps clarify which strategy may yield better results based on varying market conditions.

Limitations of the Formula

The future value of annuity formula provides valuable insights, but it has limitations. Understanding these can enhance your financial planning.

Assumptions about interest rates may not hold true. The formula typically assumes a constant interest rate throughout the investment period. However, market fluctuations can lead to variable rates that impact growth.

The formula doesn’t account for inflation. Inflation erodes purchasing power over time. If you only consider nominal returns, you might underestimate the actual future value of your investments.

It overlooks taxes on earnings. Taxes can significantly reduce your net gains. Depending on your tax situation and jurisdiction, this could affect how much you ultimately retain from an annuity.

The formula simplifies payment timing. Most calculations assume payments occur at regular intervals without considering factors like early withdrawals or changes in contribution amounts. Real-life scenarios often involve complexities affecting total outcomes.

It’s based on consistent contributions. The effectiveness hinges on making consistent contributions over time. Unexpected events may hinder your ability to maintain those payments, impacting overall growth potential.

You should evaluate these limitations when using the future value of annuity formula for planning or decision-making.