Imagine navigating the complex world of finance without a reliable map. That’s where audit procedures come into play, serving as your essential guide to ensuring accuracy and compliance in financial reporting. These systematic methods help you assess an organization’s financial health while identifying potential risks that could impact its operations.

In this article, you’ll discover various examples of audit procedures that can strengthen your understanding and implementation of effective auditing practices. From substantive testing to internal controls evaluation, each procedure plays a crucial role in maintaining transparency and trustworthiness in financial statements. So, are you ready to dive deeper into the world of audits? Uncover how these practices can not only enhance accountability but also drive better decision-making for your organization.

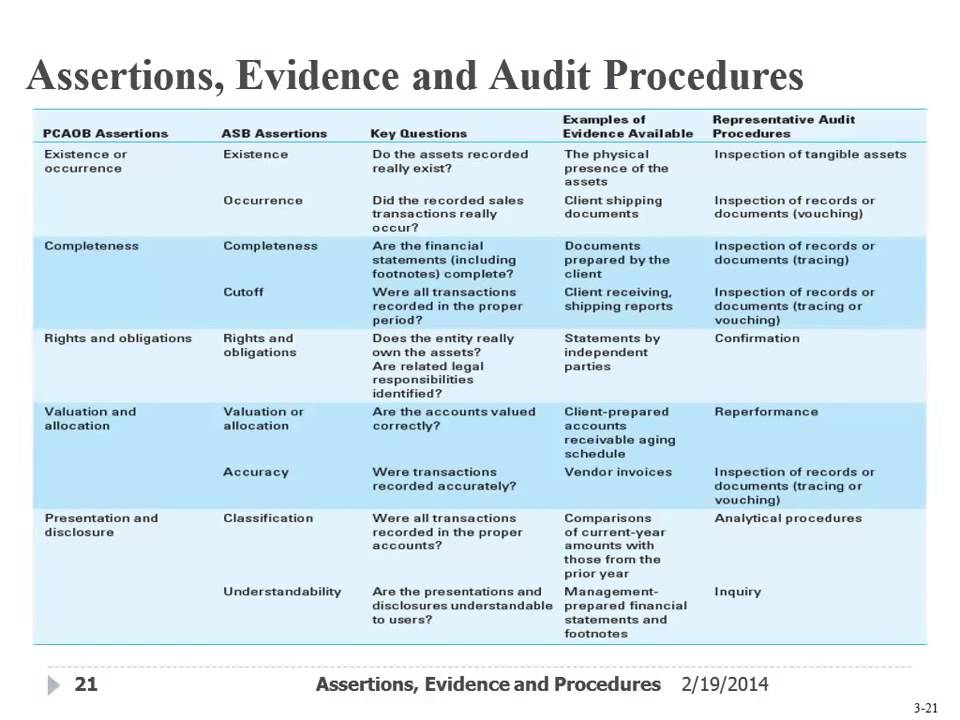

Overview of Audit Procedures

Audit procedures encompass a variety of systematic processes designed to evaluate financial statements and internal controls. These practices ensure that organizations remain compliant with applicable laws and regulations. Here are some key examples:

- Substantive Testing: This involves testing individual transactions within financial statements. Auditors check for accuracy by verifying information against supporting documents.

- Internal Controls Evaluation: Auditors assess the effectiveness of an organization’s internal control systems. They identify weaknesses that could lead to errors or fraud.

- Analytical Procedures: This method uses comparisons and ratios to identify unusual trends or discrepancies in financial data. It helps auditors spot potential issues quickly.

- Compliance Testing: Auditors verify adherence to laws, regulations, and policies. This ensures that the organization operates within legal boundaries.

These audit procedures play a crucial role in enhancing transparency and accountability within organizations. Would you consider how these methods contribute not just to compliance but also to informed decision-making?

Types of Audit Procedures

Audit procedures are crucial for identifying potential financial discrepancies. They ensure the accuracy and reliability of an organization’s financial statements. Here’s a closer look at two primary types of audit procedures.

Substantive Procedures

Substantive procedures focus on verifying financial transactions and balances. These actions provide direct evidence regarding the correctness of reported figures. Common examples include:

- Confirmations: Sending requests to third parties to verify account balances.

- Tests of Details: Examining individual transactions against original documentation, such as invoices or contracts.

- Analytical Review: Comparing current period data with prior periods or industry benchmarks to identify anomalies.

These methods strengthen the credibility of financial reports.

Compliance Procedures

Compliance procedures assess adherence to laws, regulations, and internal policies. They’re essential for ensuring that organizations operate within established guidelines. Key examples encompass:

- Regulatory Compliance Testing: Evaluating if an organization meets specific legal requirements, such as tax obligations.

- Policy Adherence Checks: Reviewing whether internal controls align with company policies and standards.

- Training Records Review: Ensuring employees have received necessary training on compliance-related issues.

Steps Involved in Audit Procedures

Audit procedures consist of several essential steps that ensure a thorough evaluation of an organization’s financial health. Each stage plays a significant role in confirming compliance and accuracy within financial reporting.

Planning the Audit

Planning is crucial for effective audit execution. You must identify the scope, objectives, and resources needed. Key actions include:

- Assessing risk: Evaluate areas with higher risks to tailor your approach.

- Developing an audit plan: Outline procedures and timelines for each phase.

- Communicating with stakeholders: Ensure all parties understand their roles and expectations.

By setting a solid foundation during planning, you enhance overall effectiveness.

Conducting Fieldwork

Fieldwork involves gathering evidence through various means. This step is where most hands-on auditing occurs. Important activities include:

- Performing substantive tests: Verify transactions against source documents to confirm accuracy.

- Evaluating internal controls: Assess how well systems prevent errors or fraud.

- Conducting analytical procedures: Analyze trends, ratios, and comparisons to spot anomalies.

These actions provide valuable insights into the organization’s financial practices.

Evaluating Audit Findings

After fieldwork concludes, evaluating findings becomes paramount. This process helps determine whether conclusions align with expectations. Essential aspects include:

- Analyzing collected data: Review evidence for reliability and relevance.

- Documenting results: Create detailed records of findings to support conclusions.

- Preparing reports: Summarize outcomes clearly for stakeholders’ understanding.

Through careful evaluation, you ensure transparency and accountability in financial reporting.

Importance of Audit Procedures

Audit procedures play a vital role in maintaining the integrity of financial reporting. They ensure accuracy and compliance, which are essential for stakeholders. For instance, substantive testing verifies individual transactions against supporting documents, confirming that reported figures reflect reality.

Compliance procedures also matter significantly. They assess adherence to laws and regulations. By performing regulatory compliance testing, organizations can identify gaps in their practices, thus preventing legal issues.

Another example is internal controls evaluation. This process examines the effectiveness of an organization’s internal control systems. When you evaluate these controls regularly, you strengthen operational efficiency and reduce risks related to fraud or errors.

In addition, analytical procedures use data comparisons and ratios to uncover unusual trends or discrepancies in financial statements. If anomalies arise, they prompt further investigation into potential underlying issues.

Lastly, documentation is crucial throughout audit procedures. You should maintain clear records of findings to enhance transparency and accountability within your organization. Consistent documentation supports informed decision-making by providing reliable evidence during audits.

By understanding these examples, you recognize how audit procedures contribute to overall organizational health and trustworthiness in financial reporting practices.

Challenges in Implementing Audit Procedures

Implementing audit procedures presents several hurdles that organizations often face. These challenges can significantly impact the effectiveness of the auditing process.

Limited Resources create obstacles in conducting thorough audits. Many firms operate with tight budgets and insufficient personnel, which hampers their ability to allocate adequate time for comprehensive audits.

Complex Regulatory Environments further complicate the situation. Compliance with varying regulations can be overwhelming, especially when requirements change frequently. Organizations must stay updated on laws to ensure adherence.

Lack of Training among staff can lead to ineffective audits. If your team lacks knowledge about audit processes or standards, it may result in overlooked risks or errors during evaluations.

Data Management Issues also pose significant challenges. Disorganized financial records can obstruct auditors’ efforts to verify information accurately, leading to potential discrepancies in findings.

Cultural Resistance within an organization might impede audit implementation. Employees may view audits as intrusive rather than constructive, resulting in reluctance to cooperate fully during the process.

Addressing these challenges requires strategic planning and investment into training and resources, ensuring that your organization successfully implements effective audit procedures while maintaining compliance and transparency.